| Programme Dates | Last Date to Apply | Programme Fees |

Venue |

|---|---|---|---|

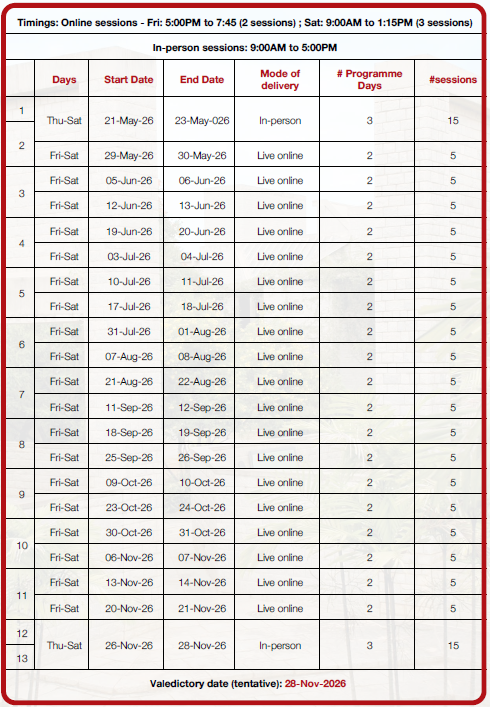

| Start Date : 21-May-2026 End Date : 28-Nov-2026 |

1-May-2026 |

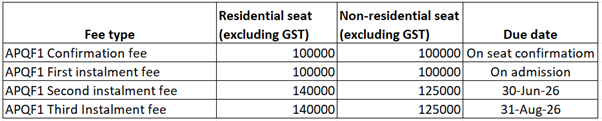

Rs. 4,50,000/- (Non-residential, excluding GST) Rs. 4,80,000/- (Residential, excluding GST)

|

Blended mode – Combination of IIMB Campus & live online |

Last date to apply: 1-May-2026

Programme commencement date: 21-May-2026

Programme end date: 28-Nov-2026

Ms Ranjini K S

Email: ranjini.ks@iimb.ac.in

Ph: 080 2699 3264 / +91 8951974080

Participants who successfully complete the program will be granted IIMB EEP Alumni Status. For more details on EEP Alumni and the benefits, click here

Advanced Programme in Quantitative Finance (APQF) blends mathematical and statistical techniques with financial markets using practical examples and hands on market applications. It will prepare participants with practical financial market quantitative applications along with theory behind the models & methods. The program will utilize market software products and packages such as Bloomberg to produce market scenarios in financial instrument pricing and risk measurement. The participants will get equipped with software techniques used in econometric modelling, Quantitative Finance Models and Machine Learning. Participants will produce applicable results while working on their capstone project.

Program Objective

| 1. Market Microstructure | Global Capital Markets – FX, Fixed Income, Credit, Commodities • Marketplaces – OTC and Exchanges • Trading Mechanics |

| 2. Basic Econometrics | Statistical Models and Market Data • Primer on Econometric Models • ARMA to GARCH Models • Curve Bootstrapping Techniques (SOFR) • Volatility Models – Implementing GARCH • Market Spreads and Correlations |

| 3. Theory of Financial Instruments | Cash and Derivatives Instruments • FX and NDF • Bonds – Sovereigns, Corporates, Inflation Linked • Bond Forwards • Forwards, Futures, Swaps • Vanilla & Exotic Options • CDS, TRS, CLO |

| 4. Valuation Models | Pricing Models – Deterministic & Stochastic • Closed Form Models – Linear Instruments • Simulation Models – Non-Linear Instruments • Pricing a Spread Option • Model Comparison and Selection |

| 5. Financial Instruments | Detailed mechanics of instruments – cash flows & sensitivities • Pricing and Greeks |

| 6. Financial Instrument Design with Bloomberg | Bloomberg Built-in Instruments • Swaps and Options • Custom Instrument Design • FX & Interest Rate Structures |

| 7. Financial Instrument Payoff Scripting | • Design a Custom Financial Instrument • Bloomberg Scripting Interface • Payoff Logic & Structures |

| 8. Financial Instrument Analytics | Hedging & Risk Management • Derivatives Book Analytics • Book Management Basics |

| 9. Trading & Sales Desk Management | • Hedging in the Marketplace • Quoting Pricing Levels • Sales & Trade Management • Hedge Cost & Credit Charge • CSA Agreements |

| 10. Model Risk | • Model Risk Framework • Risk Measurement & Minimization • Model Validation |

| 11. Machine Learning | Introduction to Machine Learning • Approaches & Models • Applications to Financial Markets |

| 12. Accounting | Accounting of Derivatives Book |

| 13. Capstone Project | Design a Financial Instrument or Book Analytics with Valuation |

Programme Directors

Sankarshan Basu is currently a Professor in the Finance and Accounting Area at Indian Institute of Management Bangalore (IIM Bangalore). He has been at IIM Bangalore since 2002. Between August 2022 and September 2023, he was also the Dean, Amrut Mody School of Management (AMSOM), Ahmedabad University while on leave from IIM Bangalore. At IIM Bangalore, Sankarshan has been the Chairperson of the Post Graduate Programme in Public Policy and Management (between April 2017 – March 2019), the Chairperson of Career Development Services (between April 2012 – March 2015) and Chairperson of Alumni Relations (between January 2007 – September 2011) at IIMB.

A part time programme certificate of completion will be awarded by IIMB to participants upon successful completion of the programme and satisfying programme requirements.

Sample Certificate:

Note: Certificate image is for reference to potential participants only and may change at the discretion of Executive Education Programmes Office

The programme fee is payable in three instalments as per the following schedule:

Please Note: *Please add GST at prevailing rates to the programme fee.